Personal finance isn’t one-size-fits-all—because it’s personal.

The way I manage my money might look completely different from how you manage yours, and that’s okay. Why? Because our goals, dreams, and visions for life are different. We all have unique values, priorities, and paths—so it only makes sense that our financial plans would reflect that.

That said, while no two financial journeys are exactly the same, there are some foundational tips and steps that apply to everyone. Let’s dive into those.

Step one? Get clear on your goals.

What does your dream life look like in 1, 3, 5, 10, or even 20 years? If you’re in a relationship, sit down with your partner and dream together. Talk about what you want your future to look and feel like—because you need a destination in mind before you can map out how to get there.

Once you have your vision, it’s time to assess your current reality.

That means tracking your spending. I know—it’s not the most glamorous task. But trust me, it’s essential. You can’t improve what you don’t understand, and you need to know where your money is actually going.

I recommend tracking every single dollar you spend for at least three months. Yes, every dollar. After that, you’ll have a clear picture of your spending habits and can decide whether you want to continue tracking or if you’ve gained enough insight to move forward with intention.

Be sure to check out this blog post on 5 Things You Should Cut form Your Budget for ideas on what to cut. https://jesswaynecoaching.com/5-things-you-should-cut-from-your-budget/

Next, it’s time to create your Financial Mission Plan.

Think of this as more than just a budget or spending plan—it’s a comprehensive roadmap that includes your financial goals, debt payoff strategy, and savings plan. But what really sets it apart is that it goes one step further: it aligns your spending with your values.

Too often, we say certain things are important to us, yet our spending habits tell a different story. I want that to change for you. I want your Financial Mission Plan to reflect what truly matters in your life—so your money is working for you, not against you.

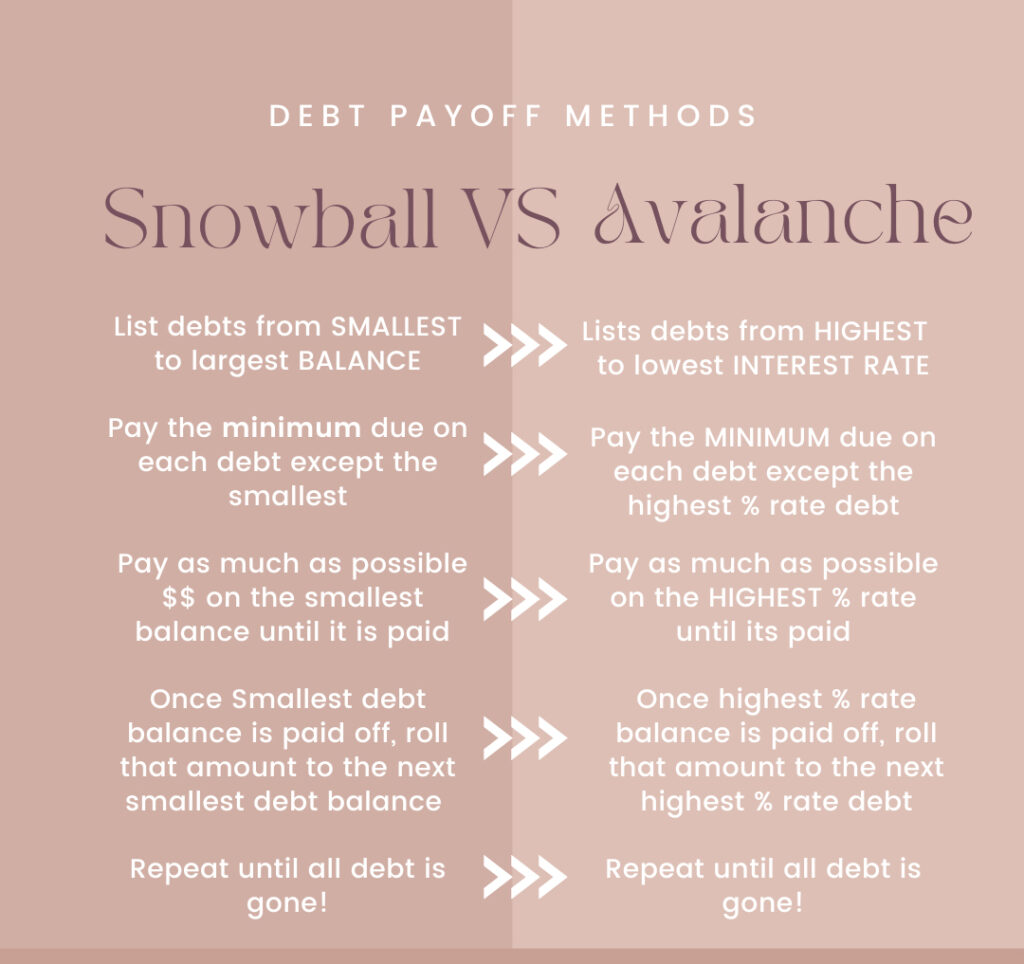

You will want to focus on paying off your high-interest rate debt.

Yes, the snowball method can be a great way to build momentum with some quick wins—but if you want to save the most money in the long run, prioritizing your high-interest debt is key.

That’s why I typically recommend the avalanche method, especially if you have debt with interest rates higher than 7%. By tackling that high-interest debt first, you’ll pay less in interest over time—and that extra money can be put toward savings or even spent guilt-free!

Aim to Save 3-6 months’ worth of expenses into your emergency savings fund.

Yep, this can be a lot of money waiting to be spent in case of an emergency, but let me tell you, you will be so grateful when an emergency happens, because it will, and you have money set aside to float you through it. Whether it’s a job loss, a medical emergency, a sick child, or an unexpected injury, having that financial cushion means you can focus on what really matters—without the added stress of wondering how you’ll pay for it.

If you typically spend $5k per month in expenses your fully-funded emergency fund will be $30k. Make sure this is liquid money, meaning you can get your hands on it within a few business days. This will make sure you don’t use debt during an emergency situation.

You can pay off your debt WHILE building your emergency fund. Yep, you don’t have to be completely debt-free before you add money to your savings account. You can do them simultaneously.

Plan ahead for future expenses.

This is where your financial goals and vision for your life become incredibly important. Maybe you want to take an annual, debt-free family vacation like I do. Or perhaps your goal is to retire early, or design a spending plan that lets you live frugally now so you can contribute more to your retirement.

Planning ahead for known expenses is key—things like Christmas, back-to-school shopping, summer activities, or even your annual Costco membership. These aren’t surprises, so let’s stop treating them like they are. Prepare now so you’re not caught off guard later.

If owning a lake house or a boat is part of your dream, then it’s time to ask yourself—how much do you need to save each month to make that a reality? What steps will it take to get there, whether it’s purchasing a pontoon or a fishing boat?

This is your moment to shine. Start planning ahead, saving intentionally, and taking consistent action toward those goals. Your dream life won’t build itself—it starts with the decisions you make today.

Create your Financial Mission Plan to allow you to enjoy your money NOW and in the FUTURE!

This is a balancing act, to be able to enjoy your hard-earned money both now and during your ‘golden years’. Are you saving enough for retirement? Am I spending too much now? I want to make memories with my kids while they are little but we have so much debt.

If you are needing some help figuring out just how to balance your finances to meet all your goals, head to Jesswaynecoaching.com for more information on my resources, courses, podcast, and 1:1 Financial Coaching Program. I’d love to help support you with this journey to financial freedom.

xoxo

Your Financial Freedom Coach- Jess Wayne